The Derivatives of DeFi

The most popular form of derivative in DeFi and the crypto space as a whole is the inverse perpetual swap, pioneered by BitMex back in 2016.

Trading “perps” allows a user to get synthetic exposure to an asset through futures with no expiry. The stand out feature of a perp is the funding rate which is paid or received when in a position where the price of the future is at a premium or discount to the spot price of the traded asset. When funding is positive, longs pay shorts (typical in a bull market). When funding is negative, shorts pay longs (bear market things).

A popular strategy to earn yield utilising perps was to short and asset when funding was positive, and long the same asset on a spot exchange to achieve a delta neutral position. This resulted in very juicy yields during the bull market. In bearish conditions this strategy is much less profitable and incurs higher risk as it tends to be longer tail assets that have positive funding for shorter periods of time.

Perps are an incredible instrument for achieving high leverage trading.

The Rise of the Perp

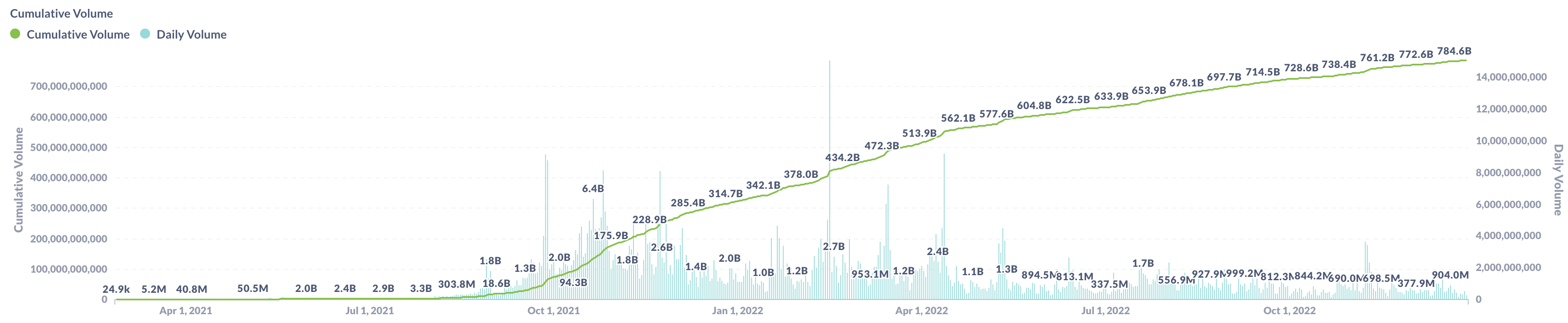

DyDx has and continues to dominate the decentralized derivative space since they launched their perpetual swap DEX. At the time of writing it has settled over $784 billion in less than two years. A growth rate set to surpass that of Uniswap in 2023.

Derivatives in legacy finance dwarf the volumes of spot markets. I would expect this trend to follow through into DeFi as the UX improves with time.

The volumes have dwindled in the bear market as can be seen in the volume profile above. Ultimately perp instruments benefit massively from bullish conditions.

DeFi Options

The Real Yield

Options have seen increased adoption across the DeFi space. They allow traders to express their views on the market in a huge range of ways, taking into account among other things; price changes, time and volatility of the underlying asset. Understanding and utilising options is massive skill upgrade that can benefit a trader in so many ways.

Option sellers can earn yield on their underlying assets if the option they sell expires out of the money. This is one of the most utilised forms of yield in traditional finance and was ported over to decentralized finance by the team at Ribbon Finance in the form of the decentralized option vault (DOV).

DeFi Options growth

Options in traditional finance make up the majority of the derivative trading.

In DeFi, options have been growing, but much like their CEX counterparty, Deribit, they are a behind in terms of volumes and users vs the behemoth that is the perpeutal swap. Options are a little more complex than the perpetual swap and the UX has a long way to go to compete with the likes of DyDx.

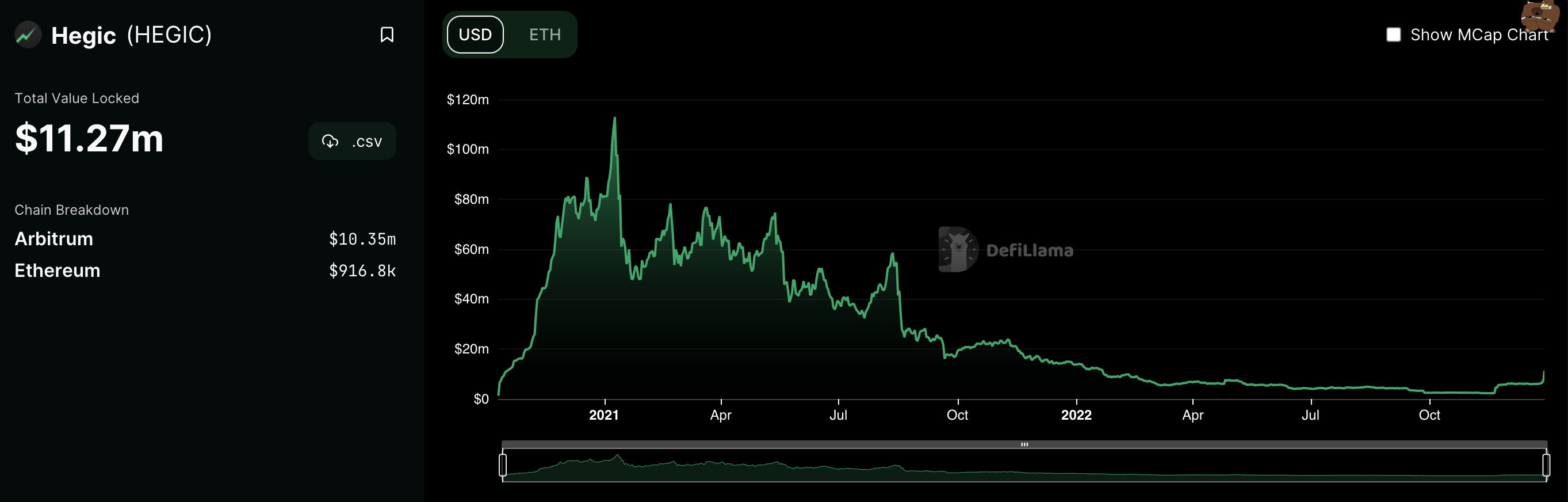

Hegic and their AMM saw some early traction back in 2020 but has since had to change ways. Perpetually selling ATM options was a losing trade for LP’s, particularly in a raging bull market.

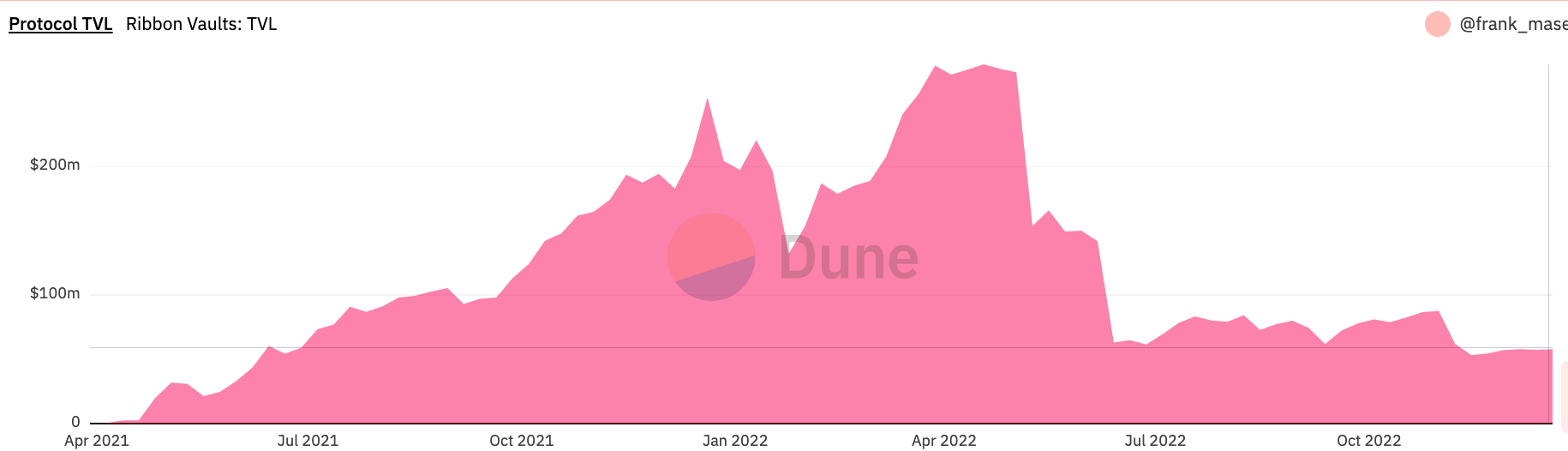

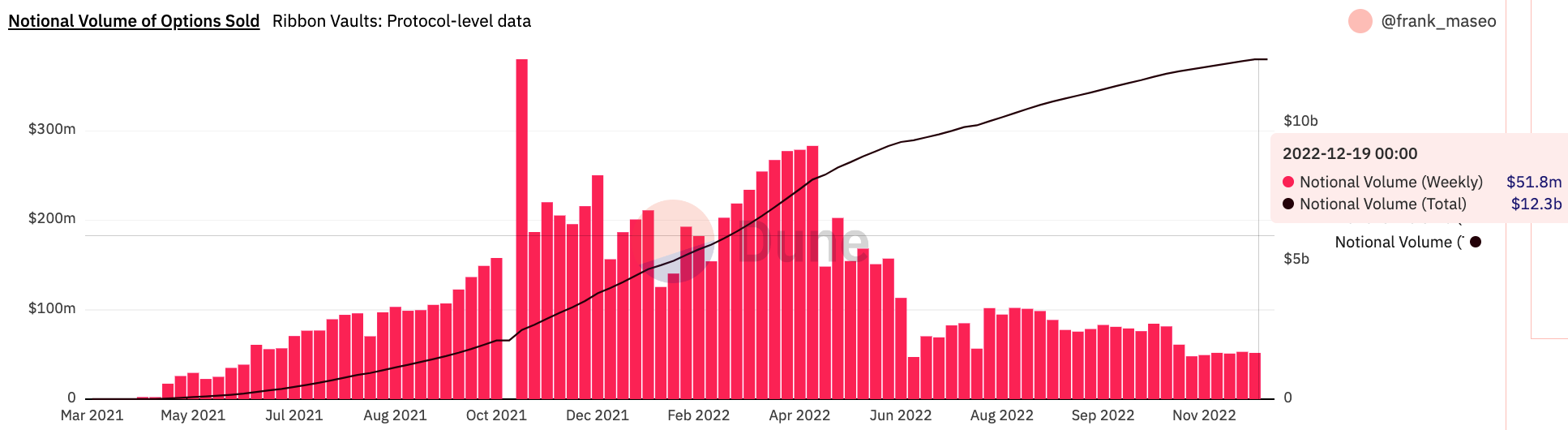

Since summer 2021, Ribbon Finance, through their DOVs have been the dominant force in option trading. Notional volumes since inception are at the time of writing a cumulative $12.3 billion. Currently this is all processed through Opyn via their o-tokens, which are auctioned off weekly to market makers. Growth has dwindled in the bear market, but there remains appetite to earn yield by selling options and more recently, exotics.

Evolution of the DOV

DOVs began as vanilla option selling strategies; selling weekly 0.1 delta calls and puts via a Gnosis auction. Vault users simply deposit their assets, market makers buy the options. Premiums are paid out up front and if the options expire ITM; the option holders collect their winnings.

Ribbon then built out their own front end for the auctions to allow for a better UX.

As sales picked up, some trends came to the fore. IV was front run as traders sold options prior to the Friday auction. This led to lower yields for vault participants. To combat this, Ribbon teamed up with Trade Paradigm to run some blind auctions which has seen yields improve significantly. Further iterations like polynomials partial collateralization and batch sales at different times/strikes on Lyra’s AMM has been one way to counteract this, although slippage can be a problem with larger sales. Ultimately Polynomial will be limited by the growth of Lyra.

Premia have went down the route of an AMM where LP’s are perpetually selling options. It remains to be seen if they can gain traction, much like Hegic beforehand.

DOVs are at a point where current further iterations are enabling smaller improvements. There have been many iterations from various projects but these have had very little effect on their growth. This could be attributed to the stage we are at in the market cycle or an inherent weakness in design.

DOVs in there current form suffer from large drawdowns when the options expire ITM. The problem is that it’s difficult to hedge a vault position, particularly in a decentralized manner. Currently most hedging is done via perps or via Deribit. This requires active, sophisticated management.

A future iteration of the DOV will involve Ribbons AEVO, and will enable a lot more strategies while improving UX for the end user.

Exotic DOVs

Principal protected vaults utilising exotic options are a consequence of the aforementioned ‘drawdown’ problem and the demand for more ‘set and forget’ vaults.

Trading exotic options are a more sophisticated form of earning yield that can be both profitable and less risky than selling vanilla calls and puts. Ribbon with their Earn suite of products and Cega are the pioneers in this field of DeFi options and I can see them gaining traction as time goes on. Opyn’s Squeeth is something to pay attention to; everlasting options are a new invention and Opyn have recently launched a USDC crab vault that could potentially compete with other option vaults.

Risk On

People like to gamble, just take a look at the growth of perps during a bull market. But options so far, within the DeFi space, has been all about sustainable yield. DeFi options have attracted a very different type of trader/investor. The yield seeker prefers lower risk while maintaining sustainable rewards. Bridging more risk taking traders could be the next stage in DeFi options development.

Conclusion

DOVs have been the key to growing options on-chain; sustainable yield has been the end goal.

The bear market is for building and the next wave of capital will flow after the foundations have been set. Further education, improvement of UX and the development of exotic options will encourage more participants in this sector.

Further growth will come in the form of participants actively buying options. Thus far (excluding Ribbon through Opyn), there hasn’t been a decentralized venue that has taken even a small slice of market share away from Deribit, the incumbent option CEX. There is certainly a demand for risk in DeFi when looking at the growth of perpetual swaps. A deeply liquid, user friendly venue for trading options might be just what is necessary to push DeFi options to the next level.