Growth of Ribbon against competitors

Growth of Ribbon against competitors

An in depth review

Ribbon Finance

Ribbon was one of the first projects to introduce structured products to the DeFi space and have consistently iterated on their products while expanding into new areas.

Product Details

THETA

Ribbon invented the decentralized option vault (DOV); where 0.1 delta, weekly covered calls and cash settled puts were auctioned off on various assets from WBTC to AAVE.

The auction process was later improved by incorporating into Paradigm’s platform, facilitating blind auctions where they consistently beat the market rates on Deribit at the time of sales.

EARN

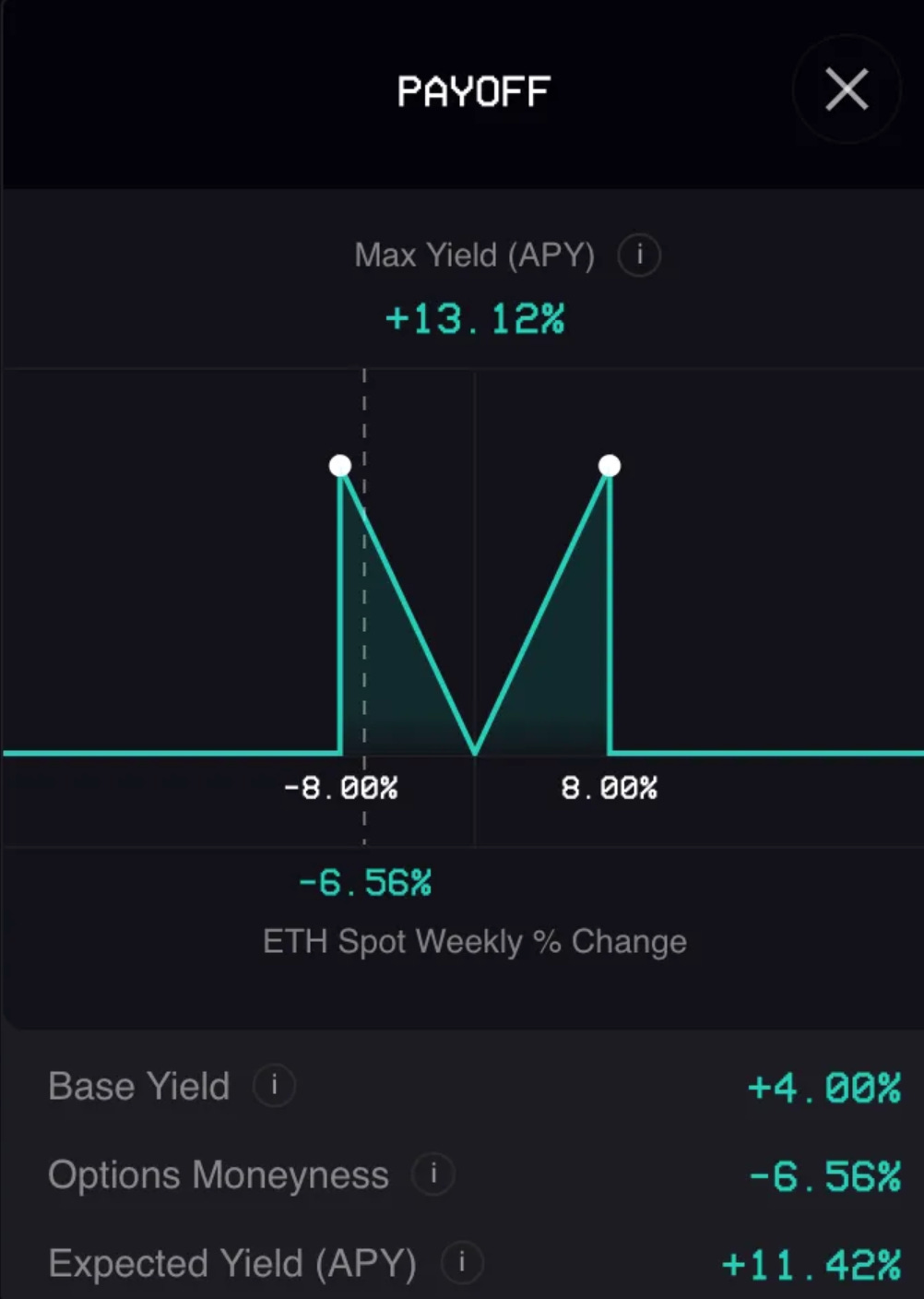

Borne out of the demand for more sustainable yield in all market conditions. Users deposit USDC into the vault where is is leant out to market makers at a dynamic rate (Ribbon Lend). Some of the yield earned is used to buy weekly ATM knock out options with an upper and lower barrier of 8%. The closer the spot price gets to the barrier the more will be paid out. If the barrier is hit at expiry, the option expires worthless. Originally participants had to lock up for 1 month at a time, currently users can withdraw at weekly intervals after the options settle.

LEND

Borne out of the demand for liquidity on the Earn product. Earn is an undercollateralized lending platdorm. The participants can choose their counter-party and deposit as they see fit based on Credora’s credit scoring, payout and intuition.

Lend brings liquidity to Ribbons Earn product allowing users to withdraw weekly as opposed to monthly.

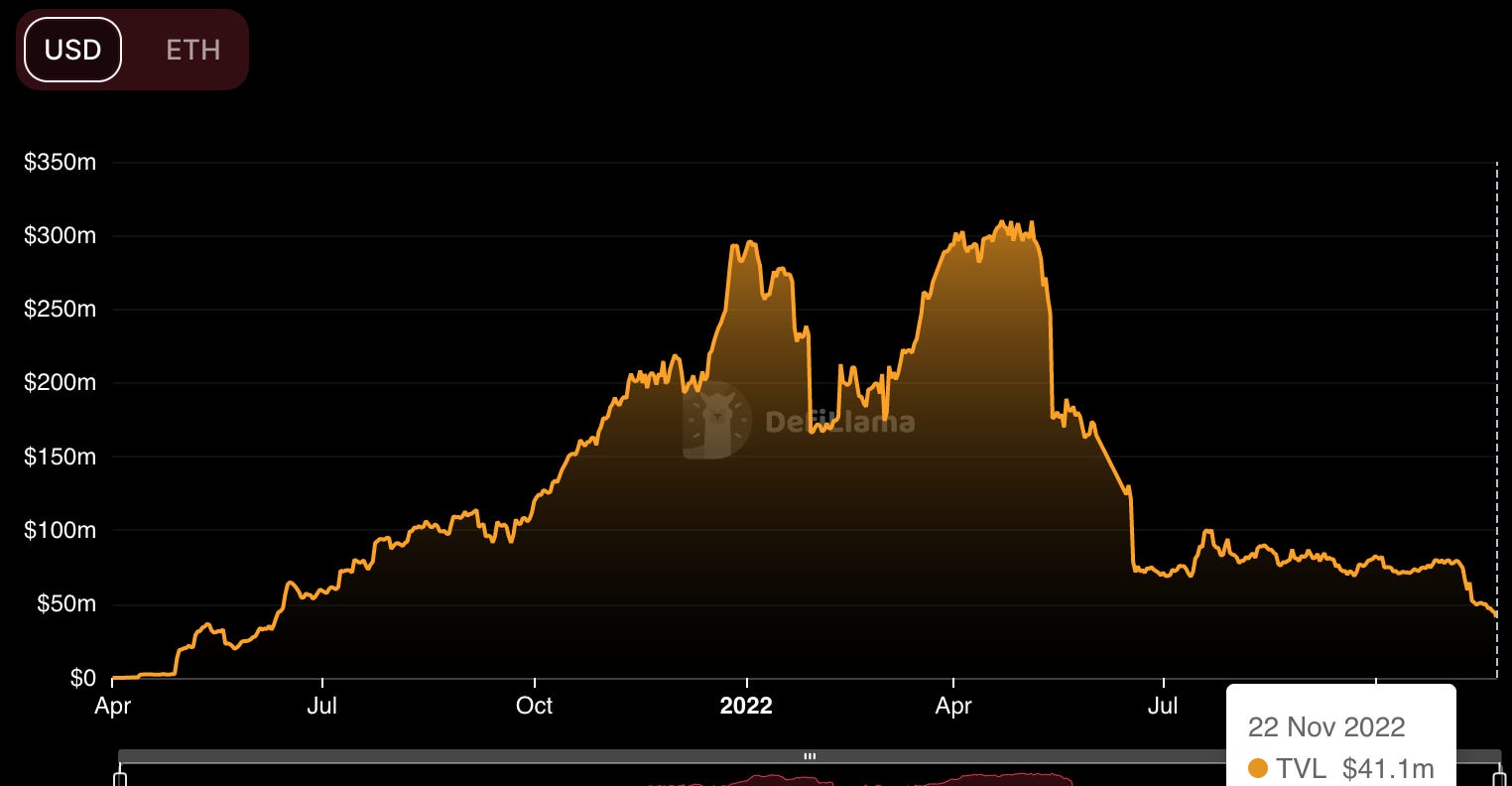

TVL

At the time of writing the TVL of all of Ribbons products is $78.59m.

Theta vaults make up 52% of the TVL at $41.1m

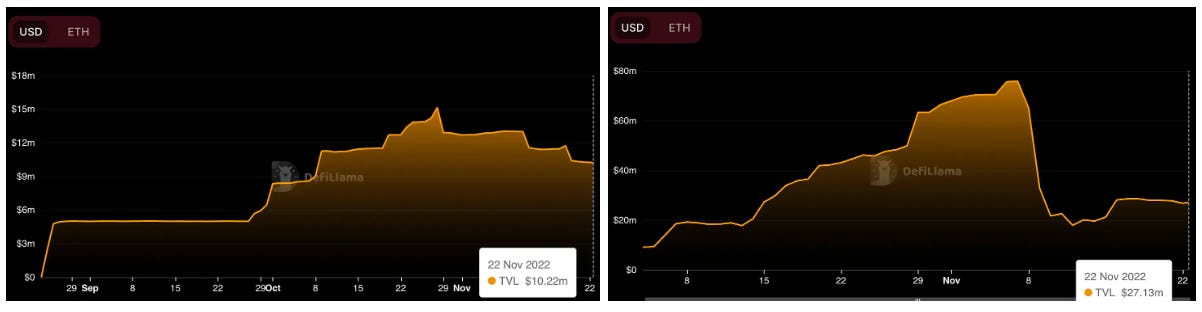

Ribbon Earn & Lend make up 13% at $10.22m and 35% at $27.13m respectively; note that they have only launched in recent months, with Lend drawing down significantly after the FTX collapse.

Performance

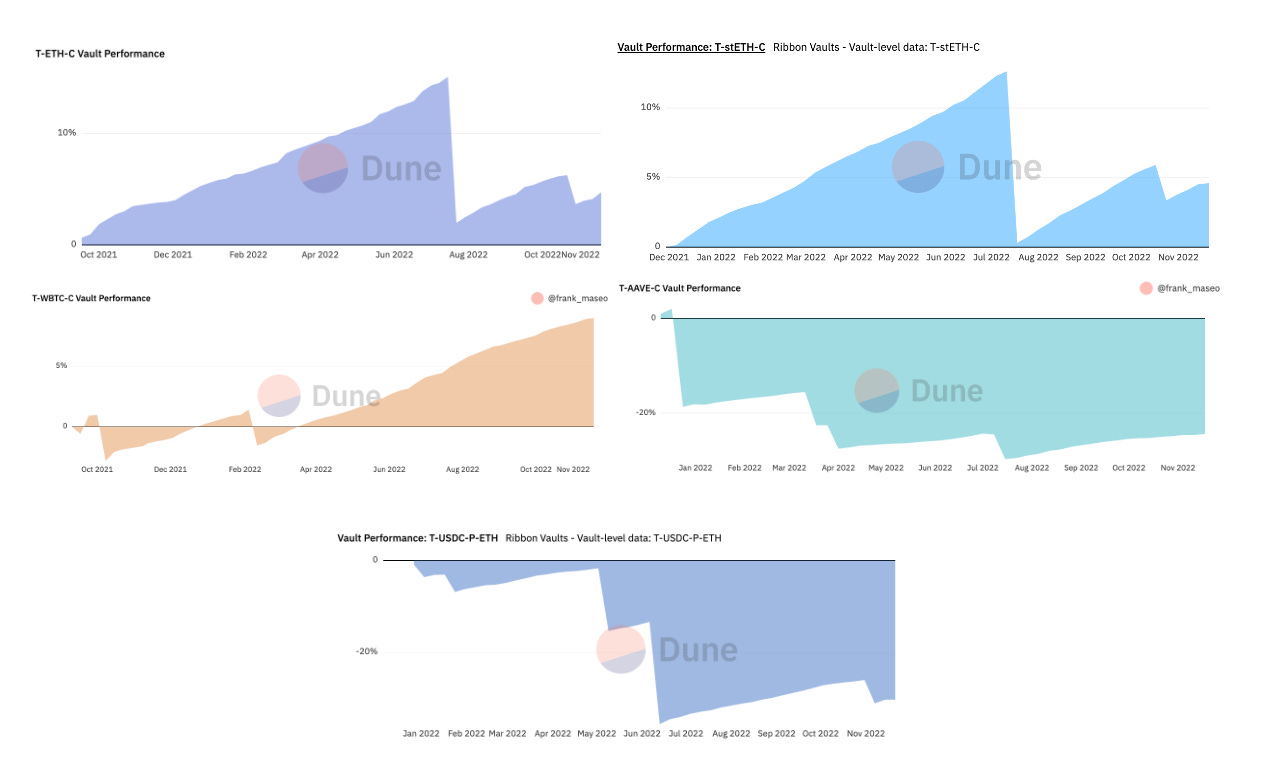

Theta

At times of extreme volatility both the covered call vaults and particularly the put selling vaults have had drawdowns. These vaults can provide a significant yield for the sophisticated participant who actively manages their positions.

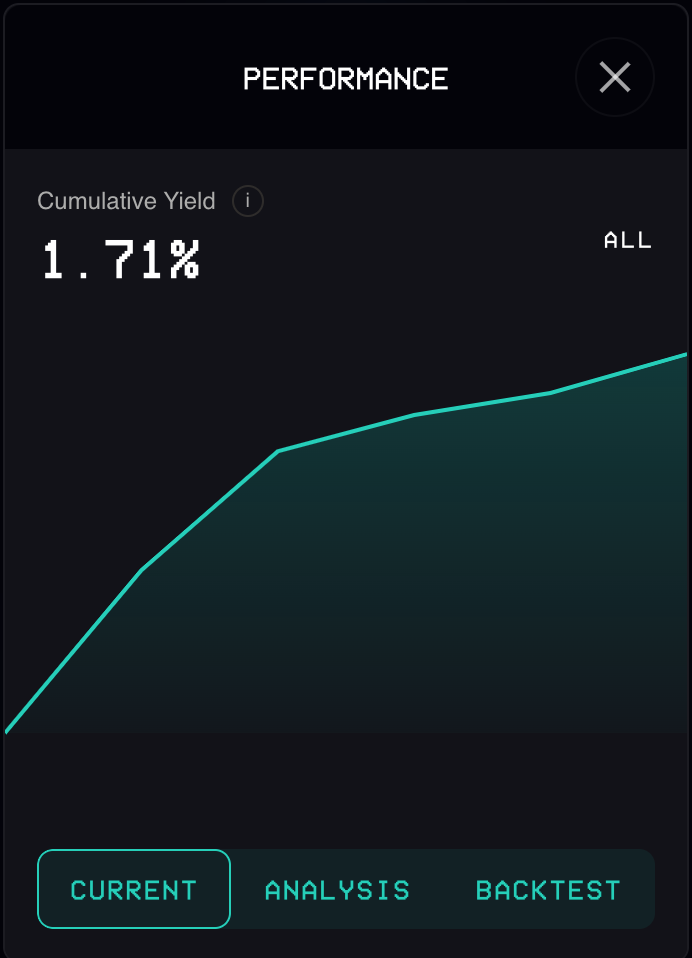

R-Earn:

The product has been live for 11 weeks now and has accumulated 1.71% yield. This annualises out to 8.41% APY compounding weekly. This can fluctuate from 4 -13.12% based on the hit rate and expiry price of the barrier options.

Addition yield in $RBN can be earned by staking and is currently yielding an extra 17% APR which can be boosted up to 2.5x by locking $RBN tokens.

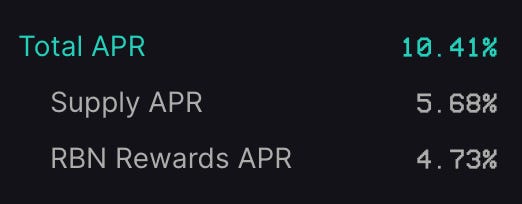

R- Lend:

The Wintermute pool is currently yielding 5.68% APR with additional $RBN tokens totalling 10.41% APR. This fluctuates based on the level of borrowing activity of the market maker.

Unique users

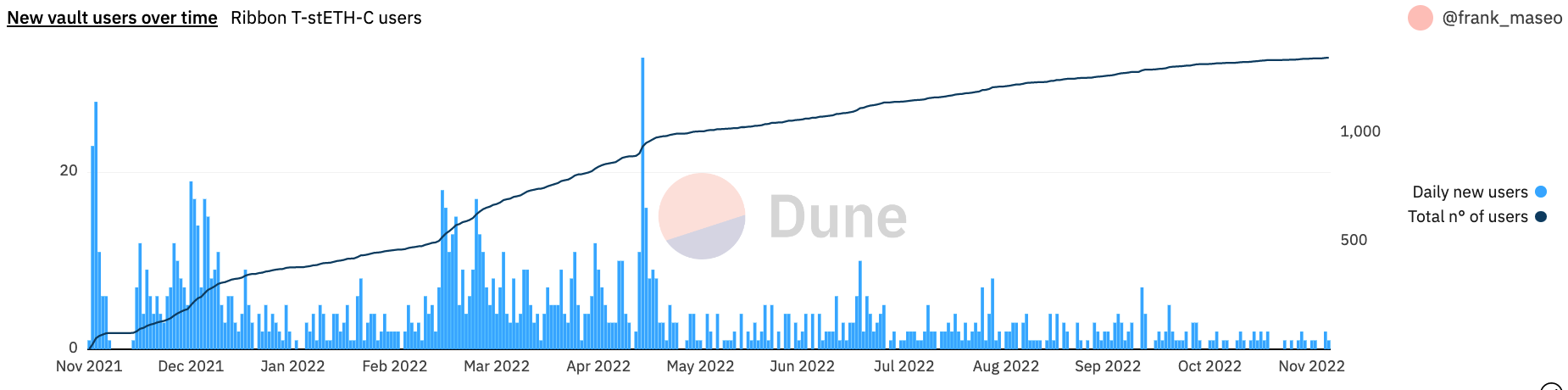

Theta

Vaults were very active during the bull market with many unique users utilising the Theta vaults. Growth has slowed as the market turned over.

The stETH vault’s growth below is indicative of the other vaults:

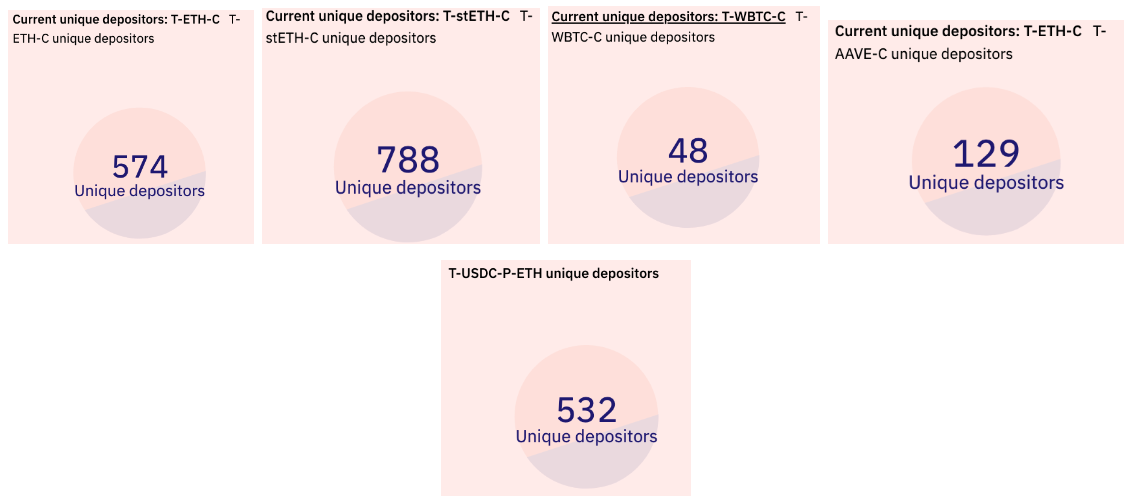

Total:

Theta: 2,071

R-Earn: 2,743

Ribbon launched a Layer3 campaign on the 3rd November which significantly boosted deposits to this product.

R- Lend:

Current holders: 1,256

Source: https://etherscan.io/token/0x0Aea75705Be8281f4c24c3E954D1F8b1D0f8044C#balances

https://etherscan.io/token/0x3CD0ecf1552D135b8Da61c7f44cEFE93485c616d#balances

Sum: 6,070

Risks

-The Theta vaults are selling options, these can expire ITM and result in drawdowns.

-Earn and Lend both have counterparty risk as the loans are undercollateralized.

-Smart contract risk

Fees

-Theta vaults take a 2% management fee and a 10% performance fee. 50% of fees get converted to ETH distributed to veRBN holders.

-Lend takes a 5% performance fee on yield earned, these fees go to the DAO treasury.

-Earn vault takes a 15% flat fee on the yield earned between epochs, these fees go to the DAO treasury.

Cega

Their V2 has recently launched removing the undercollateralized lending component.

This has decreased yields across the board but has reduced credit risk to zero.

The product currently consists of:

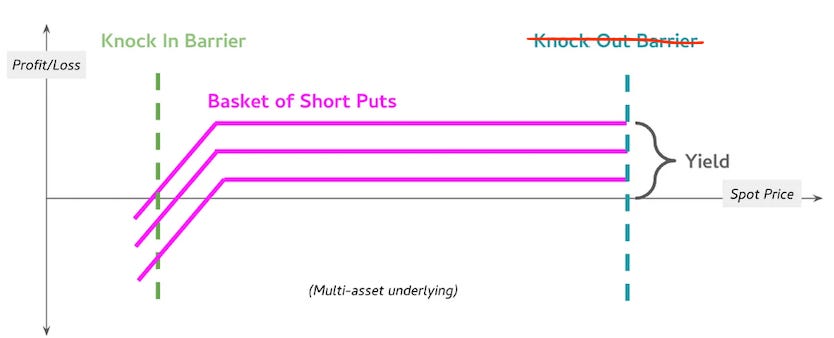

Selling exotic put options on a basket of assets to collect premiums.

At expiry, the initial deposit is returned to investors in full+premiums if the price of the linked crypto assets have not fallen by a significant amount (e.g. 50% or more)

Product Details

Every week ATM puts are sold on the underlying assets, with a lower barrier.

Cega’s products use the “worst of” options to get extra yield, selling options in BTC and ETH with riskier vaults selling in SOL and AVAX. On the expiry date, only the option of the worst performing asset will be exercised, and only then if it is in-the-money (ITM).

If the price of the underlying assets falls below the “knock in” barrier at any time, the option becomes active. If the option is still ITM by the time of expiry, the account will take a loss.

For this reason these knock in barriers are usually far below the original strike price; -90% BTC/ETH for their most conservative product.

TVL

At the time of writing there is:

The team is still working on a fix with DeFi Llama to have it tracked there.

Performance

Cega offer a variety of vaults with varying stated yields from conservative to higher risk as can be seen below.

Historically the “Cruise control”, “Genesis Basket” and “Autooilot” have performed as stated on the UI, the options sold earn a small premium and have not encountered a “knock in” event as the price is so far out. Previously they earned more than 7%APY with the additional lending component.

The “Gotta Go Fast” and “Insanic” vaults have both encountered “knock in” events and are currently down over 50% since inception.

The Supercharger vault continues to yield a high return.

“Starboard” is a new offering.

Further information can be found in this article from September and in this sheet.

Unique users

For Cega’s top vaults:

Sum: 2,084

It is important to note that Cega has been running for less than 5 months and has not yet launched a token.

Risks

-Market risk; the options can expire ITM.

-Smart contract risk.

Fees

2% management 15% performance.

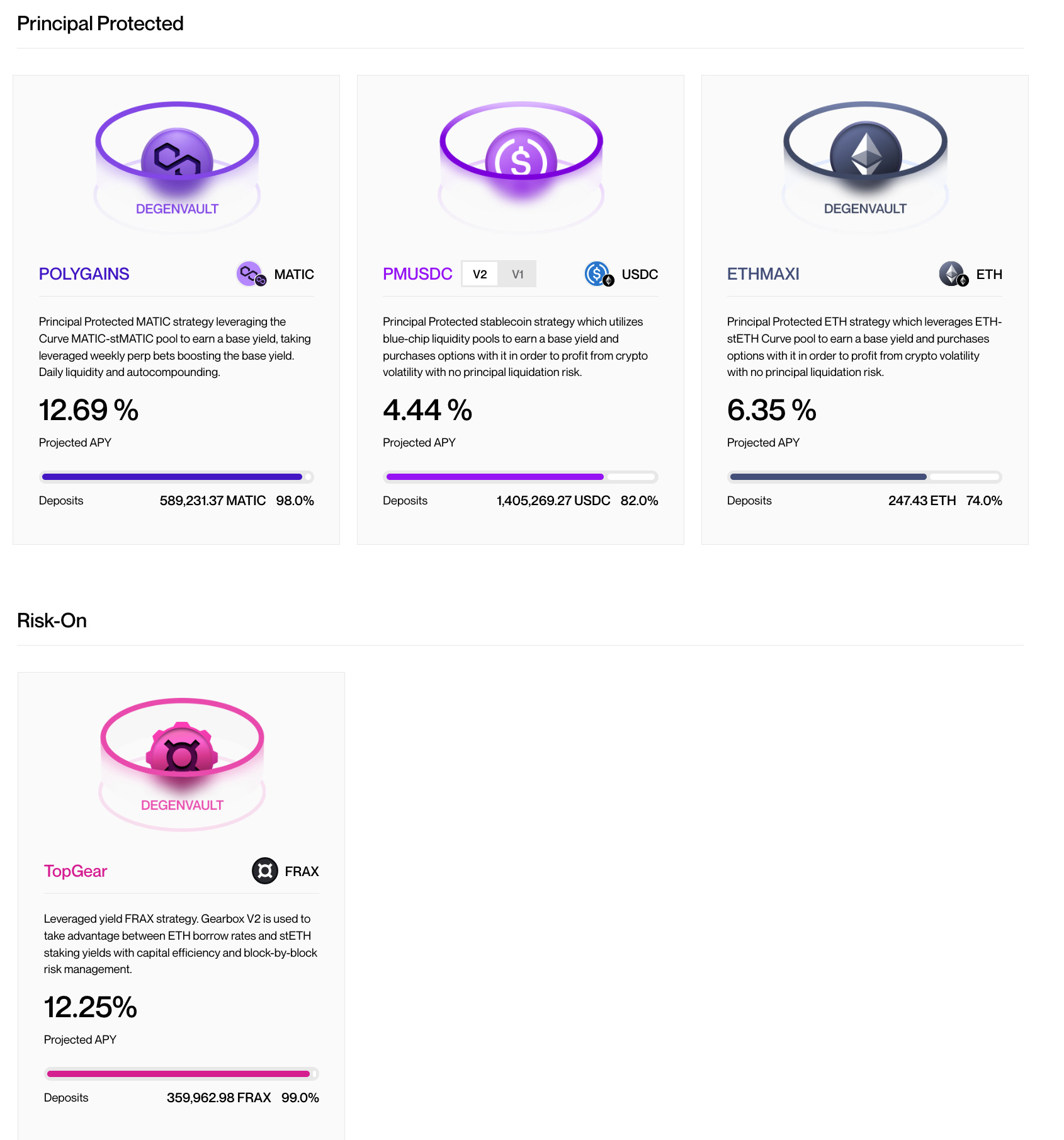

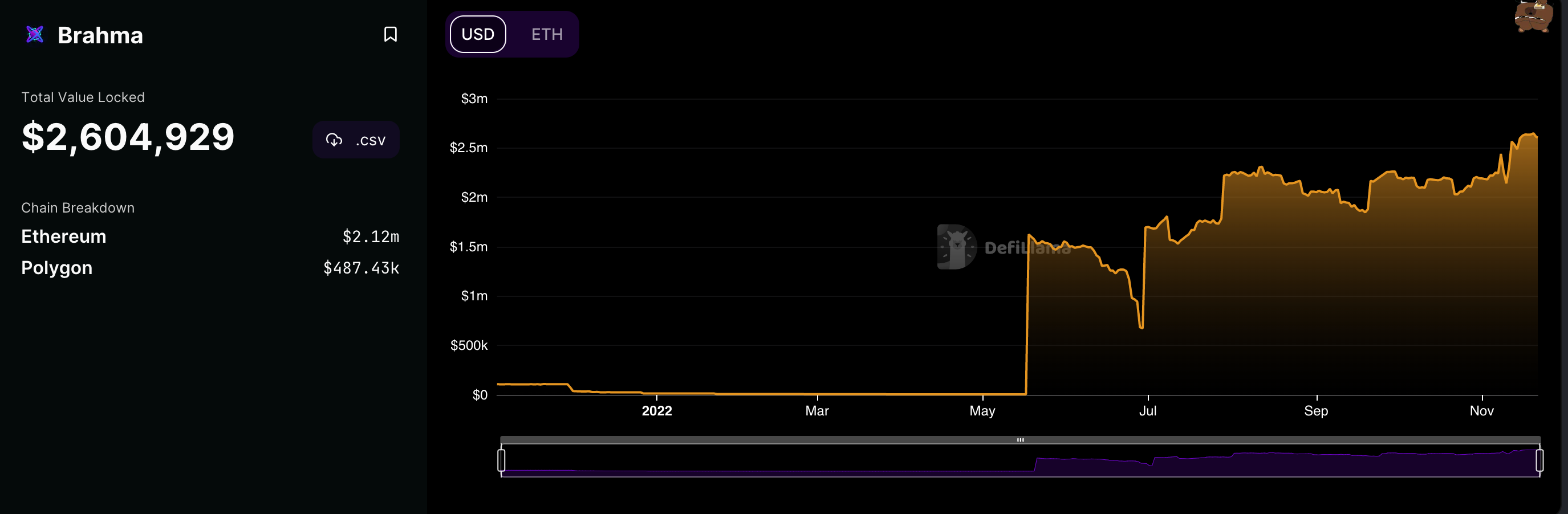

Brahma

Offering four innovative vault products, three focusing on principle protection with one riskier vault built on Gearbox:

Product Details

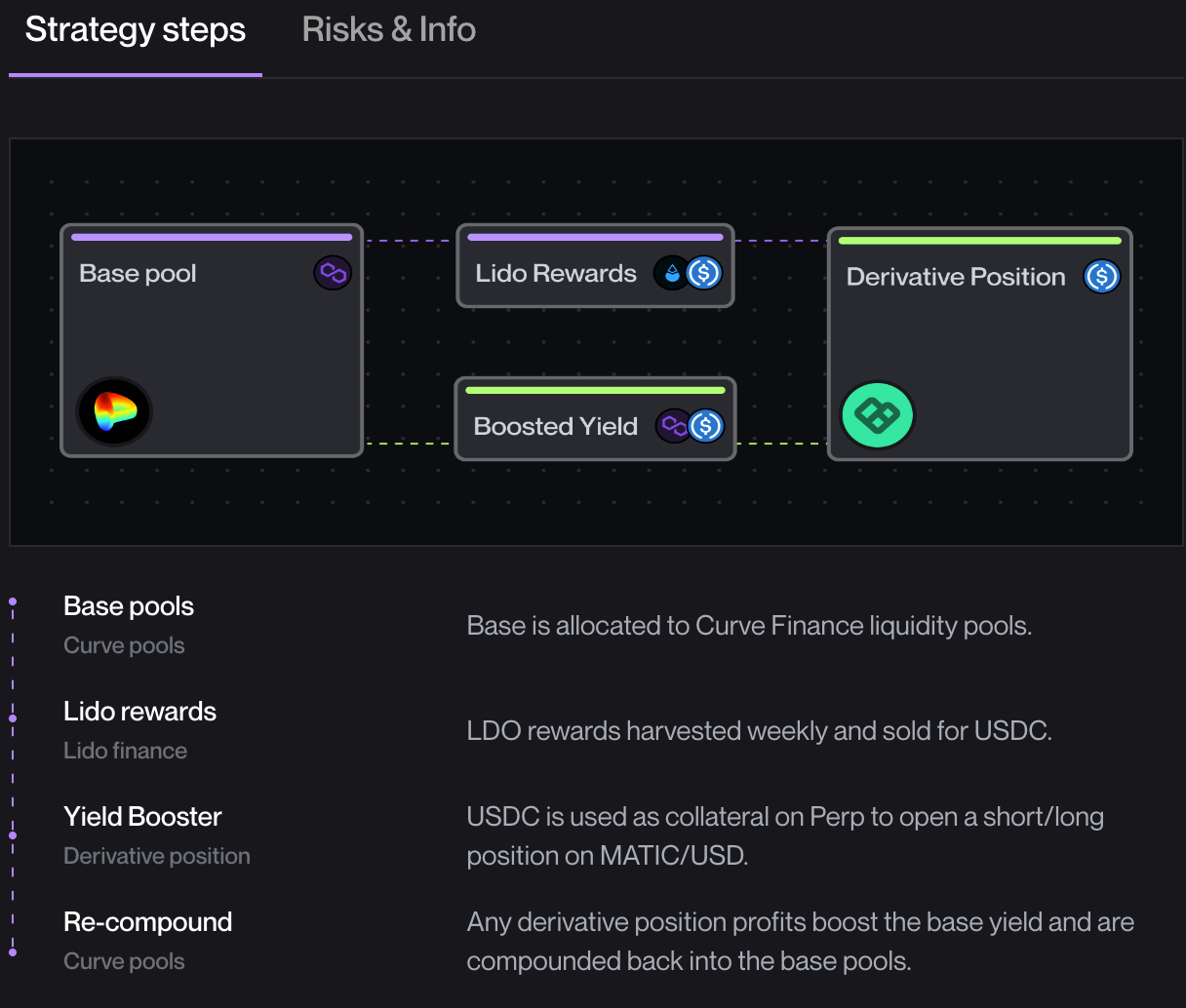

The “Polygains” strategy is laid out neatly below, and forms the basis of the other “principle protected” strategies.

The USDC harvested profits are bridged to Optimism where the derivative trades are executed on the Perpetual Protocol. The trades are 8x leverage long or short MATIC/USDC and are taken manually based on momentum indicators; stop losses are used to minimalize losing trades.

The “ETH Maxi” vault deploys deposited assets into the stETH-ETH pool on curve and LDO rewards are harvested for USDC. These yields are then bridged to Optimism where weekly options are purchased on Lyra based on momentum indicators.

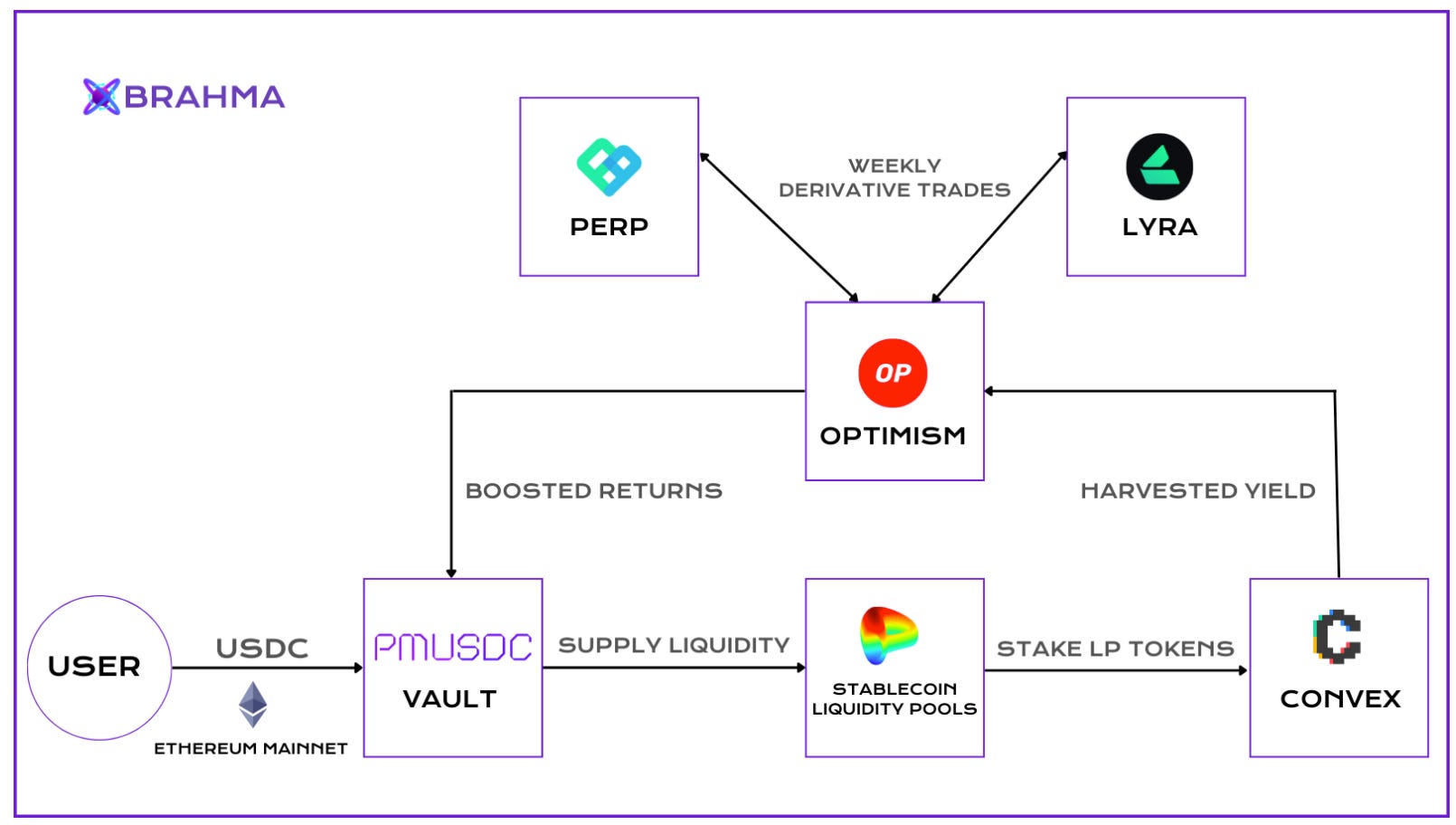

Brahama’s stablecoin pools include the PMUSDC vault (protected moonshots) and is much like the Polygains pool utilising Curve, Convex, Optimism and Perpetual Protocol.

The latest vault to launch on Brahma is built on top of Gearbox and utilises stETH applying leverage of up to 10x:

TVL

Slow and steady growth as they cap their vaults adding new products gradually.

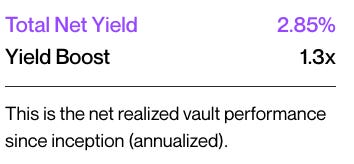

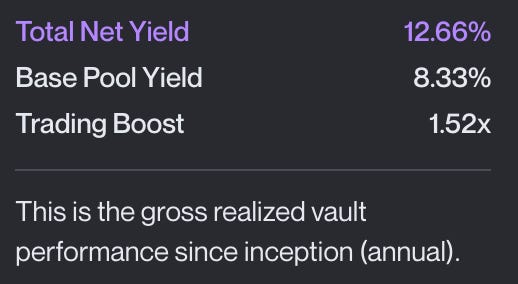

Performance

PMUSDC

Polygains

ETH Maxi

This vault is currently under development with a new version launching at some point in the future.

Current APY: 6.35%

Unique users

PMUSDC

Polygains

Capped and is currently at max capacity.

TopGear

Recently launched and is at capacity.

Risks

-Impermanent loss and realised loss if assets are withdrawn during a de-pegging event.

-Slippage when exiting the curve pools.

-Smart contract risk.

-Human error when bridging/ taking trades.

Fees

PMUSDC: 15% performance fee.

Polygains: 15% performance fee.

ETHmaxi: no fee, currently undergoing an update.

TOPGEAR: 10% performance fee, 0.5% withdrawal fee.

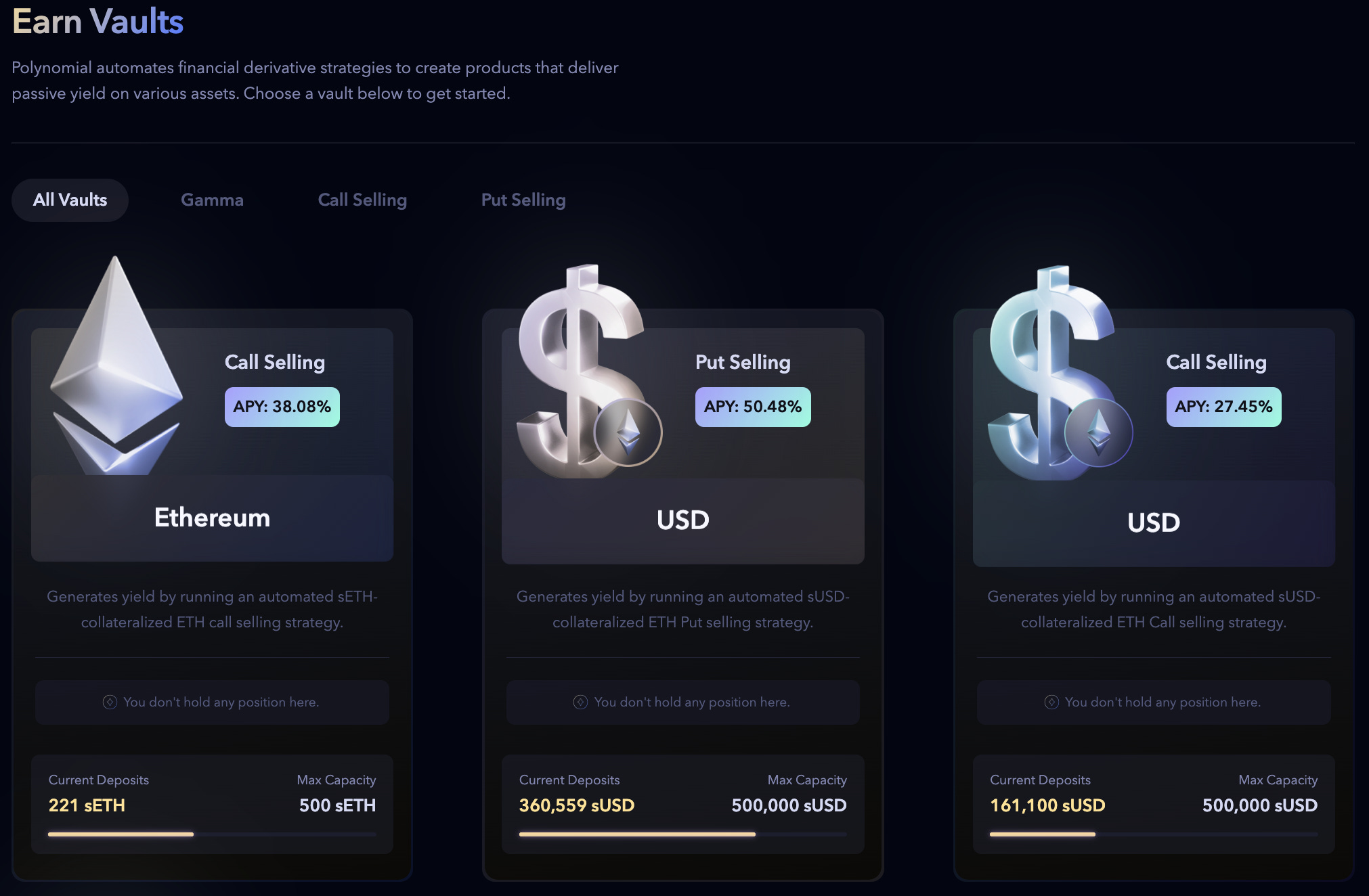

Polynomial

Product Details

A fascinating product that has iterated on the original DOV strategy featuring:

-Synthetic covered calls and cash settled puts allowing for near infinite liquidity and partial collateralization.

-Sold via Lyras AMM, allowing for more flexibility of execution (multiple strikes and dates/times) and enabling faster withdrawals (4 hours).

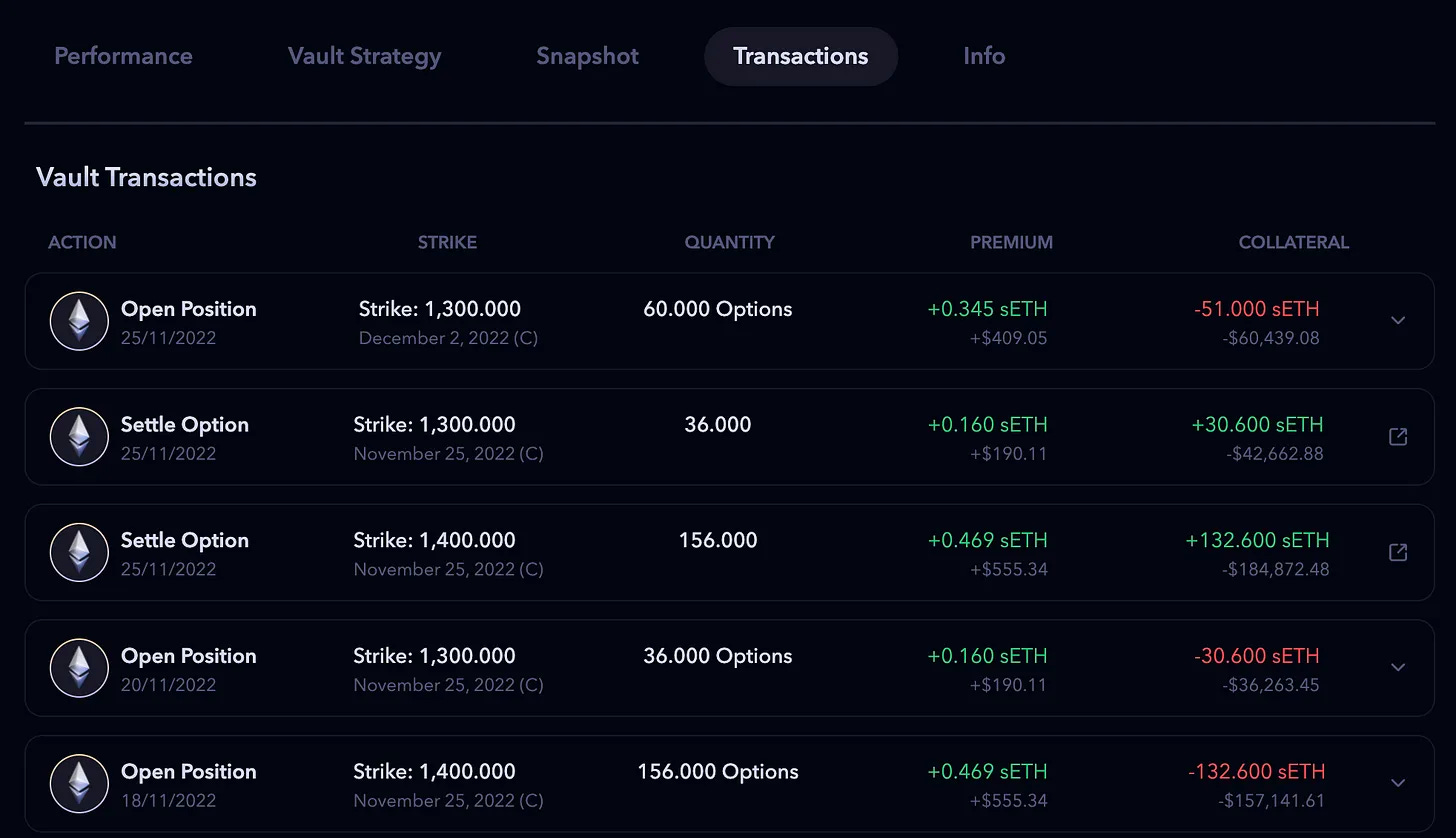

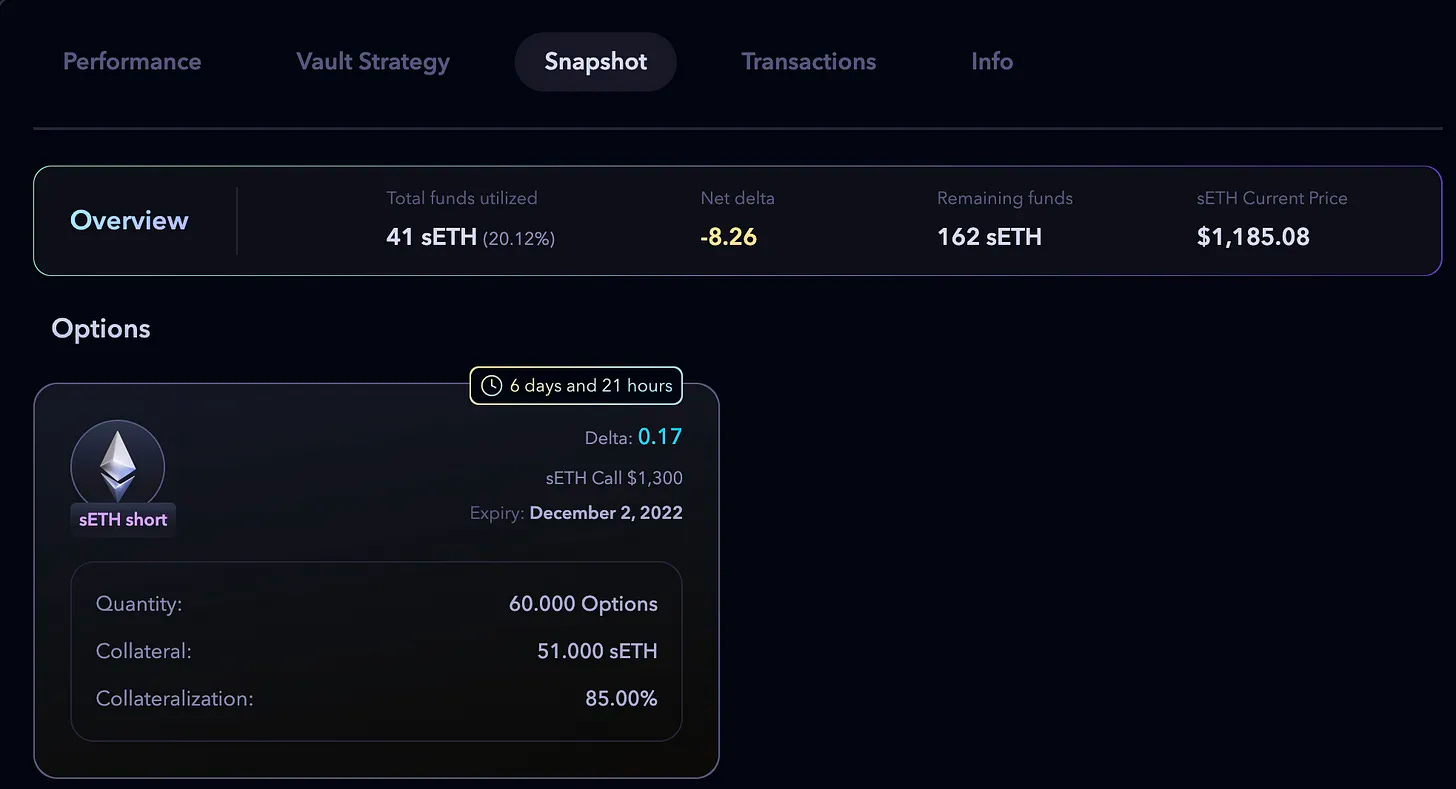

As you can see below on the ETH covered call vaults, the manager has recently sold calls on a small portion of the sETH vault at a collateralization of 85% and will aim to sell the rest of the options later in the week as can be see from the previous weeks opening and settling.

TVL

Note: vaults are currently capped to around $500k each.

Performance

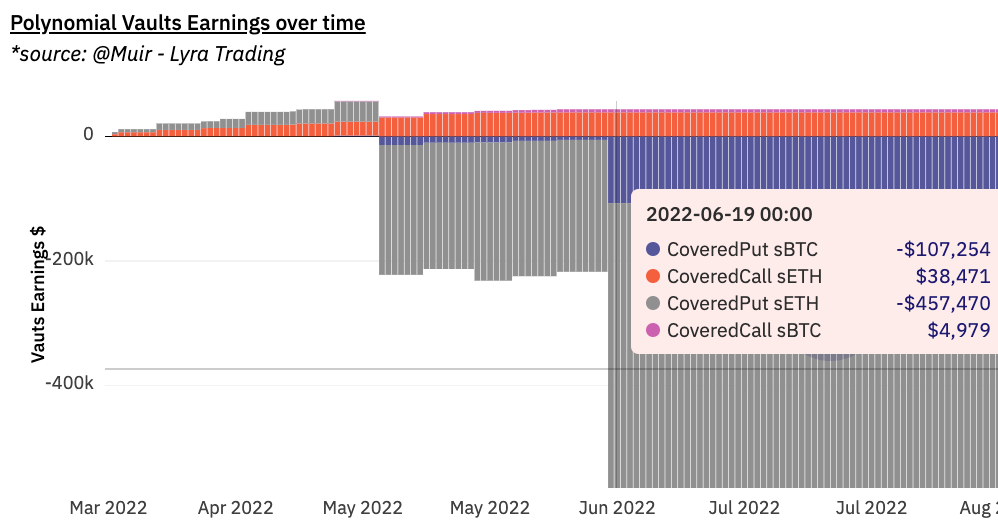

As with most DOV, there have been large drawdowns in the past.

Since August. ETH call selling vault. sETH as collateral.

ETH put selling vault, sUSD as collateral

ETH call selling vault, sUSD as collateral

The v1 vaults showed significant losses throughout 2022.

Unique users

Polynomial has a significant number of unique users. It is important to note that the protocol currently does not have a token. Since October there has been incentivization with Optimism Quests to help gain traction.

Risks

-Market risk. Options can expire ITM.

- Execution error as these vaults are manually managed.

-Smart contract risk

Fees

1% withdrawal fee and a 10% performance fee.

Conclusion

-Ribbon has dominated and continues to dominate the DOV space.

-Selling options are risky and can lead to significant drawdowns.

-High yields are available to sophisticated operators who actively manage their positions.

-When considering the numbers of users, this sector is very much in its infancy.

-Exotic options are gaining traction and showing promise.

-Potential of airdrops and other marketing campaigns can could skew usage.

Great write up, didn’t realise there were all these other DOV players!